Since my time at Microsoft (almost 20 years ago!), I have been infected by the digital identity virus. At one moment I was even part of the WEF Personal Identity workgroup. Since then, I followed the identity space in some depth, some years more than others. See also my post on The Cambrian Explosion of Identity from 2019 that also figures David Birch.

Earlier this week, that same David Birch published a very interesting post about digital identity: the bottom line of his insight is that we should be less interested in solving pre-digital conceptions of identity and more in (certified) credentials.

I recently came to a similar conclusion, but from a completely different angle.

First, I bumped into The Block Whitepaper on CBDCs (Central Bank Digital Currencies) from August 2020, and got intrigued by the schema on page 13:

The authors do a great job in explaining the difference between Claim-based (or account-based) money and Object-based (or token-based) money.

In other words, money is an asset, and can be represented as a Claim (Account) or as an Object (Token)

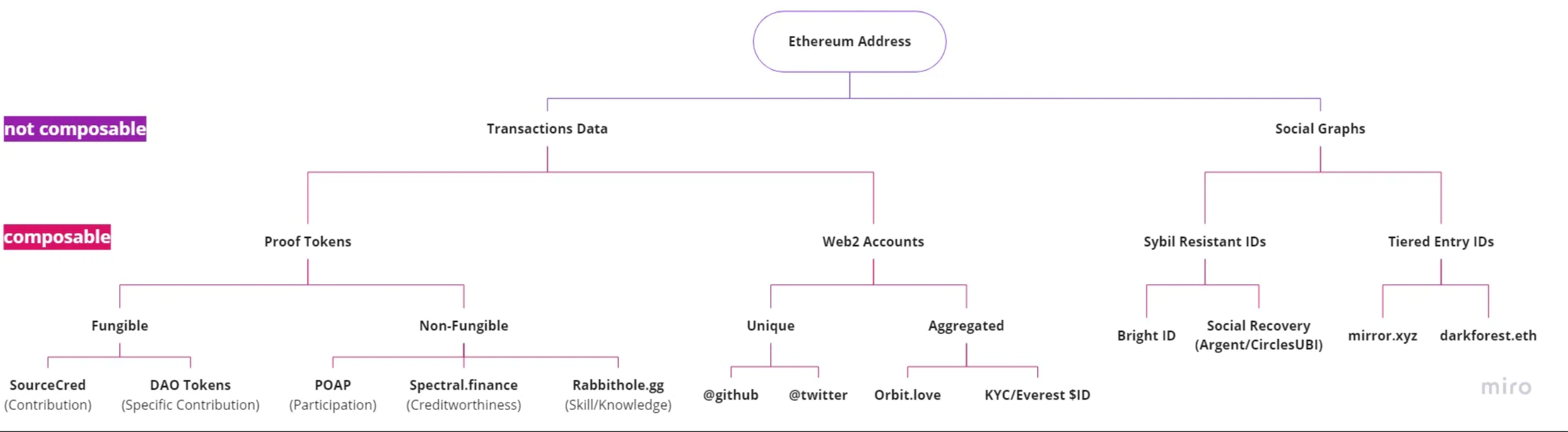

Then I ran into this May 2021 post by Andrew Hong on The Composability of Identity across Web 2.0 and Web 3.0. It’s a quite technical paper, and I probably only understand 5% of it, but my attention was again drawn to a diagram on the composable and non-composable aspects of identity:

Andrew Hong writes: “The second layer (and onwards) highlights categories and products that allow us to represent that transaction data and/or social graph as tokens. Since tokens have the qualities of existence, flexibility, and reusability – then by the transitive property – our digital identity now does as well. I can move around these tokens at will to different accounts and in different combinations.”

I suddenly realized that the difference between Account-based money and Token-based money also applied to identity.

In other words, just like money, also identity is an asset (it always was), and it can be represented as a Claim (Account) or as an Object (Token)

During my 2003 Microsoft project, I was lucky enough to be exposed to more advanced identity thinking by wise people like Kim Cameron and the other folks from The Internet Identity Workshop gang, and I got quite familiar with their thinking of certified identity claims or claims-based identity.

But only now, I realized that both Money and Identity can be account- or token-based, and that token-based is probably what’s going to help us make progress, because it makes identity and money programmable.

In other words:

For Account-based identity, you need to be sure of the identity of the account holder (the User ID / Password of your Facebook-account, your company-network, etc.). For Token-based identity (Certified claim about your age for example) you need a certified claim about an attribute of that identity.

For a paper/plastic ID Card/passport, it is the signature of yourself and the signature of the issuing authority, and plenty of other technical ways of ensuring the integrity of the card of passport (holograms, etc.). But it is a certified claim that the ID Card/passport is real, authentic, not tampered with.

In the case of an electronic ID Card (like the one we have in Belgium), the certified “token” for authentication or for digital signature is stored on the microchip of the ID card, and can be enabled by the PIN-code of the user (a bit like User ID / Password)

For a certified (identity) claim (like proving that you are older than 18 for example), you basically need a signed token, a signed attribute. And because it is done digitally, (identity) attributes becomes programmable, you can assign it access and usage rights

For Account-based money, you need to be sure of the identity of the account owner (the User ID / Password or other mechanism to access your account). For Token -based money (a 100€ bill, an NFT token, a ETH token, etc.) you need a certified claim about an attribute of that money.

For a 100€ bill it is the signature of the President of the ECB (European Central Bank) and plenty of other technical ways of ensuring the integrity of the paper bill (holograms etc.). But it is a certified claim that the 100€ bill is real, authentic, not tampered with.

For digital money, it is a signed and encrypted token representing one or more certified aspects of that money. And because it is done digitally, money becomes programmable, you can assign it access and usage rights, just like you could do for identity aspects

So, I come – although from a different angle – to the same (or at least similar) conclusion as David Birch in his latest post about identity that (certified) credentials are the way forward.

“These credentials would attest to my ability to do something: they would prove that I am entitled to do something (see a doctor, drink in the pub, read about people who a richer than me), not who I am.” (David Birch)

I am just adding the money dimension to it, and using the same sentence, I can now say:

“These credentials would attest the money’s ability to do something: they would prove that the money is entitled to do something (pay for Starbucks, pay for food, only to be used if there is enough money on my account, etc.), not whose money it is. (Petervan)

Post Scriptum:

You could also consider NFTs as certified claims of something (in today’s hype, they are certified claims of the authenticity of an artwork, but it could be anything, also identity, or also money. Amber Case for example referred to NFTs in the context when mentioning the Unlock Protocol on her ongoing overview of micropayments and web-monetization:

Unlock Protocol has a particularly inventive approach to NFTs — using them as customizable membership keys for certain sites. This allows people to set a length of time for the membership, or access to certain features like private Discord channels.

Content creators can place paywalls and membership zones in the form of “locks” on their sites, which are essentially access lists keeping track of who can view the content. The locks are owned by the content owners, while the membership keys are owned by site visitors.

In that sense we can really look at certified credentials as key to open something (a door, a website, a resource) or to enable something (a certain action, a certain right, a certain flow, etc).

My input was a “pick-and-choose” list of bullet points. You can find the full list below. My input date was 27 Nov 2016. We are now two months later, and I captured some articles/announcements related to some these bullet points. And I added at the end some additional observations. All of this should be taken with more than a grain of salt, as I dimmed my focus on FinTech since starting my Petervan Productions sabbatical on 1 Nov 2016, and don’t read/research as much as before.

As always, these are 100% my personal opinions. Sometimes provocative, sometimes innocent, sometimes the cynical view of a 60 year old incumbent, but hopefully at times contrarian and inspiring. Here we go:

+++ start 27 Nov 2016 input

In general, 2017 will be the year of illusion, delusion, and distraction for and by FinTech.

Blockchain/DLT/etc will prove itself as one of the biggest distractions of this era in that it does not solve any existing problem, maybe it solves some future problems to be identified, but with a price to pay: the price of fundamental process re-engineering. Very few will be up to this task which involves community management and regulation.

In 2017, subject to pressures on the bottom-line and macro-political forces, banks will witness massive lay-offs and disinvestments in FinTech innovation labs and initiatives. These initiatives will be re-branded as research efforts, focused solely on incremental improvements in the core business lines.

FinTech will manifest itself as a techno fantasy, drawing attention away from the real problems to be tackled: cyber-security, trust and identity, which only can be solved through laser focused industry and government efforts. No single company can solve these on their own, and self-serving patenting will be counterproductive to industry-wide success.

In the US, the Trump administration will out-regulate innovation to protect the financial institutions fiefdoms and their control of money. But despite the Trumpian rhetoric and “opportunities” for financial institutions to start playing their old extraction-value games, financial institutions will be challenged by citizen uproar to give back to society.

Despite all these negative predictions, volume and frequency of FinTech investments will dramatically increase. Like in other industries, a 100M$ Fund will be considered as peanuts. Like in traffic jams, investments become bigger and last longer. Like traffic jams, ROI will be difficult to impossible to resolve.

What I am missing in many predictions is that most are just extrapolations of existing trends. They ignore the fact that the trend can just die or become a commodity where prices trend towards zero.

What I am missing is the creative/opportunity orientation (what do you want) vs. the reactive/responsive orientation (what problem are you trying to solve).

The way we think about change, disruption, and transformation) or whatever you want to call it) is going to be completely different in 5 years time. The speed of change is so big that our thinking is getting disrupted. The underestimated and ignored exponential power in all of this is the “power of networks”. I have another post in preparation for that, but in the meantime I would invite you to get familiar with following books and thinkers:

The Seventh Sense: Power, Fortune, and Survival in the Age of Networks, by Joshua Cooper Ramo

Whiplash: How to Survive Our Faster Future, by Joi Ito

The Inevitable: Understanding the 12 Technological Forces That Will Shape Our Future, by Kevin Kelly

Trillions: Thriving in the Emerging Information Ecology, by Peter Lucas, Joe Ballay and Mickey McManus (already from 2012, but so advanced in its thinking)

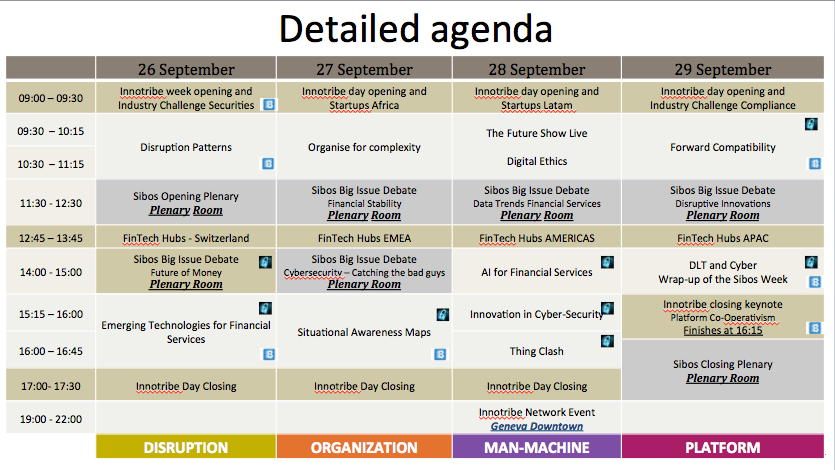

Two weeks ago, I shared with you a high level preview of the Innotribe Sibos 2016 programme.

As promised, I will reveal more details for each day in some subsequent blog posts leading up to Sibos week 26-29 Sep 2016 (37 days left at the time of this writing).

Our preparations are in full swing. We are in the midst of a series of intense prep calls with all speakers, together with our production teams and our facilitators and designers. All engines are on!

It has always been our intention to build a program with architectural integrity and a week of intense learning experiences. This year is no different.

General structure:

General overview of the Innotribe Sibos 2016 programme

The structure of the week program is fairly straightforward:

We start every day with an opening of the day

We close every day with a closing of the day

Over lunch time, we have spotlight sessions by several FinTech hubs: one day for Switzerland, one for EMEA, one for the AMERICA, one of APAC

For the opening session, the Innotribe team will welcome you, and for the Monday opening, we will zoom in into some highlights of our Innotribe Industry Challenge on Securities (about issuing a bond on the blockchain).

Our day anchor will then walk you through the plan of the day. Our day-1 anchor is Michell Zappa from Envisioning Tech, Brazil. He will come back in the day closing to wrap up the learning of the day.

In between we have several Innotribe sessions. We don’t do anything during the plenary big issue debates so you have the time to enjoy those as well.

The main theme of Innotribe day-1 is “disruption re-defined”. We have three sessions:

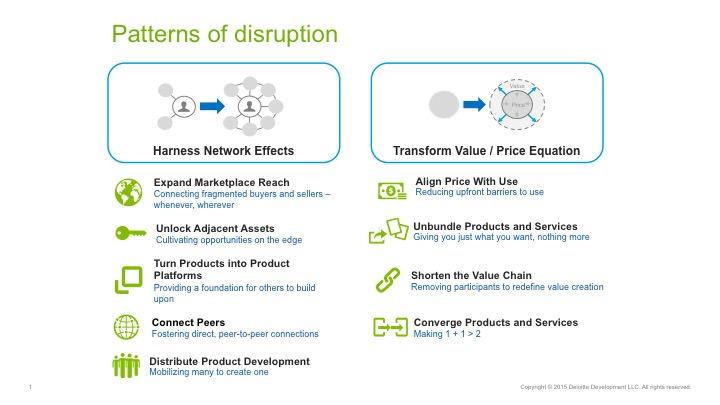

Patterns of disruption in wholesale banking

The Future of Money

Emerging technologies for financial services

Patterns of disruption in wholesale banking

Learn to anticipate and react to disruptions in Securities, Trade Finance and FX.

Begin 2016, the Deloitte Center for the Edge published a deep research on nine patterns of disruption cross-industry. Upon our request, Deloitte created a special version for Innotribe Sibos on the relevance of these disruption patterns for financial services, and how incumbents can/should react to them.

Key take-aways of this session will be:

Reframe the notion of disruption

Understand there are patterns of disruption

There is a way to be more rigorous in understanding and anticipating disruption

There are some effective ways to respond to disruption in a purposeful way

Apply these insights to our world of wholesale banking and think of specific action steps that can be taken by our organisations

The rock-star line-up for this session:

John Hagel, Co-Chair, Deloitte Center for the Edge

Val Srinivas, Research Leader, Banking & Capital Markets, Center for Financial Services, Deloitte

This is a highly interactive session, with assignments for the audience, to help you internalise the knowledge you picked up from our speakers. At the end of the session, there will be a “gift” to take with you.

The Future of Money

For the first time, this ever-popular Innotribe session has been promoted as a full-blown “Big Issue Debate” in the main plenary room of Sibos.

The idea behind Future of Money is to essentially act as a crystal ball, examining the large shaping trends that are going to affect financial services in typically two to three year’s time.

Moderated by Udayan Goyal, Co-Founder and Managing Partner of Apis Partners and Co-Founder and non-executive director of Anthemis Group, this year’s Future of Money is set to discuss the Internet of Things (IoT) and how the collection of data in our highly networked world through sensor-based technology is set to change how we think of financial services.

Other topics include the rise of artificial intelligence (AI), with decisions regarding investments and creditworthiness becoming the purview of automated systems based entirely on inputs of personalised data.

The line-up:

Jon Stein, CEO Betterment

Carlos Menendez, President, Enterprise Partnerships, International Markets, Mastercard

Amber Case, Cyborg Anthropologist and Fellow at Harvard Berkman Klein Center

We also tried to re-invent a bit the flow of a big issue debate and “sweat the technical asset” we have at our disposal. Expect more from Innotribe 😉

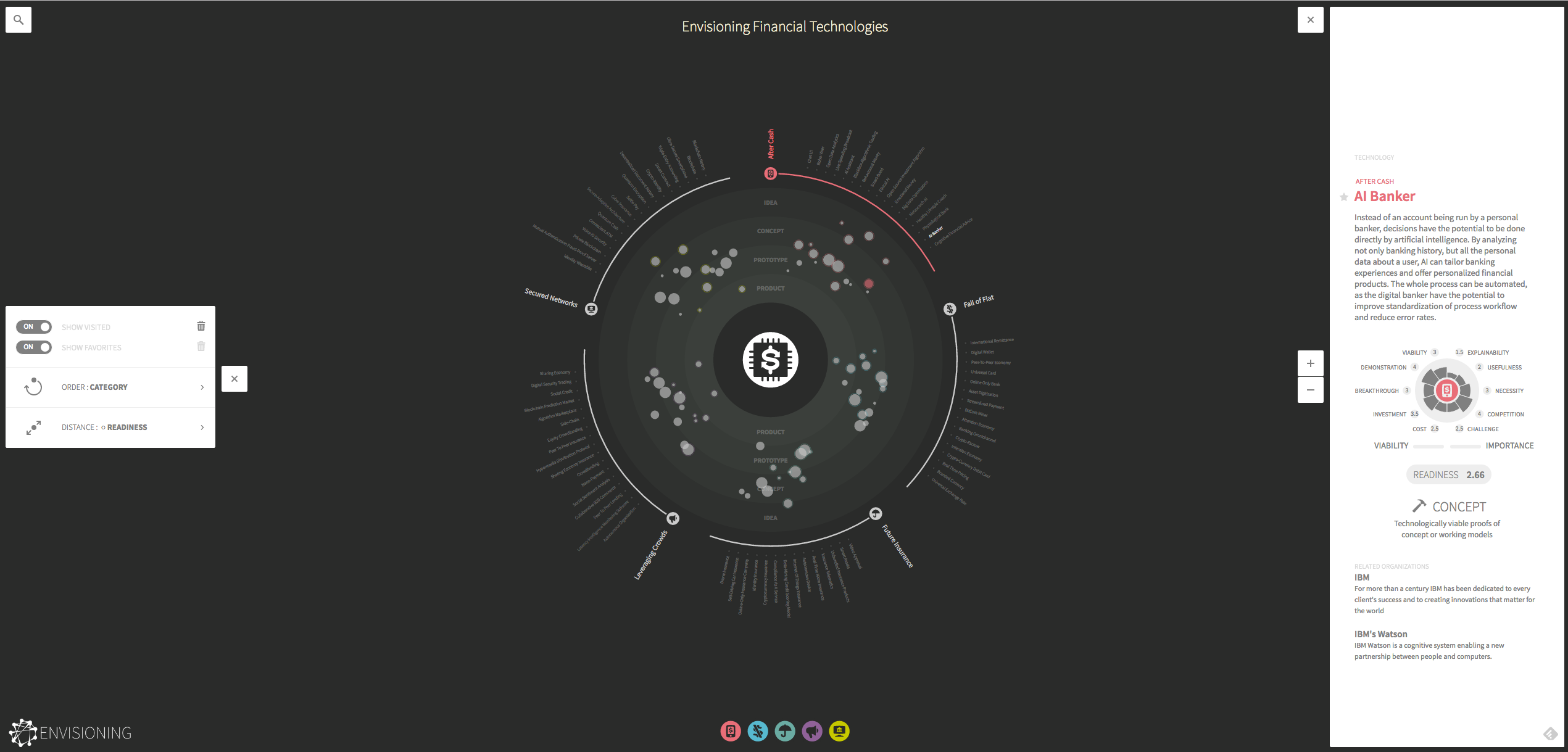

Emerging technologies for financial services

In this session, we will share the results of a research commissioned by Innotribe to Envisioning Tech from Brazil. Again, original research and a word premiere of a fantastic visualisation tool.

The different technologies will be mapped on different time horizons, and we will highlight the inter-connections between them.

Every technology will come with a navigation card detailing its relevance to the financial services industry around 10 different impact vectors – with a focus on cyber-security and distributed ledger technologies.

Screenshot of beta-version of visualisation tool

The session is animated with a spectacular screen-wide interactive visualisation.

The session is an interactive workshop with a card-game interaction with the participants. Seats will be limited.

General

All sessions are designed to maximise the immersive learning experiences of our guests. We use professional facilitators and designers to enable great group interactions. And we have an amazing audio/visual kit and production team to make the content come alive.

The pepper and salt comes from our “instigators” who have a designed role to provoke the critical discussion. The “instigators” of day-1 are:

Patrik Havander, Nordea

Anthony Brady, BNYM

Matthew Grabois, BNP Paribas Securities Services

For the sessions where it makes sense, we also have a transversal anchor for Cyber-security and one for DLT. They stay in the Innotribe space for the week, and will report back at the end of the week:

Our Cyber transversal anchor is Bart Preneel, University of Leuven

Our DLT transversal anchor is Andrew Davis, advisor from Sydney

Next week, we will cover the themes and sessions of day-2 of Innotribe Sibos 2016.

Many use the term “disruption,” to describe the upheaval we’re seeing in the financial services industry. But I believe we are witnessing a “phase-change”—a deeper transformation of how banking and business in general are done, caused by the fragmentation of everything and an unprecedented and unsurpassed period of evolutionary innovation–what might be called a “Cambrian explosion”.

With a couple of weeks from Techonomy 2013, now I think we need to get back to our human sense of analog time.

We see the Net-driven fragmentation of work and hierarchies, even as sovereign states are stealing data and intruding into systems worldwide. We see the fragmentation of trust, privacy, and secrecy. Our organizations are no longer vertically integrated but fragmented into orchestrators of highly specialized functions, sourced from a diverse group of both incumbents and aggressive newcomers.

We need stories about the humans we try to reach and move—narratives, as John Hagel puts it so well in Edge Perspectives–that have a beginning, middle, and end and convey a clear purpose and call for action and progress.

At the same time, we see an explosion of nodes on the grid, with trillions of “things” joining the digital conversation; an explosion in the volume and types of data. Digital currencies are erupting with decentralized and distributed models. States engage in surveillance and companies deploy what Jaron Lanier calls “Siren Servers”: online powerhouses that betray our trust for profit. In banking, we see the advent of network-only banks, and peer-to-peer money exchange solutions like Paypal’s Cash solution–a simple way to email money between people.

Value is being redefined, and many are rethinking what constitutes real wealth and wellbeing, beyond money and GDP. We have to rethink how we measure wealth. Robert Kennedy said: “GDP measures everything…except that which makes life worthwhile.” Happiness Indicators like Bhutan’s Gross National Happiness, the OECD’s Better Life Index, and the UK’s Happy Planet Index are already helping the world define well-being and wealth beyond money. The H(app)athon Project www.happathon.com wants to go one step further by “hacking happiness,” and shifting the world’s view of value beyond the lens of GDP.

In the financial industry, “shareholder value” and “profit maximization” remain the main criteria for investment. Nevertheless, new investment trends are emerging as a result of global changes and new ways of thinking. Investors are starting to look for criteria beyond maximizing profit, shareholder value, and pure financial return.

We have to think about what may in fact be intangible assets, along with how to account for them and invest in them. We have to re-assess the role financial markets play or should play, and their future “design principles,” so that over time we can develop more transparency, self-empowerment, and permissive not restrictive organizations.

Recently, Michell Zappa http://envisioning.io/money/ published a fantastic piece of research on “The Future of Money” documenting recent changes accelerating transactions, leveraging crowds, undermining fiat currencies, and explaining how banking is evolving into just a layer, embedded invisibly in many sorts of daily conversations. These phase changes pose fundamental questions about the role and identity of networks, institutions, and individuals.

Zappa’s timeline infographic is illuminating.

The phase-change from centralized to decentralized to distributed networks is shifting how power is distributed: from favoring the connected few to an irregular distribution that favors some individuals, and to a horizontal distribution of power that favors the whole of the network.

We seem to live in a state of perpetual crisis, jumping from one incident to another, with no room to reflect or to assess. It feels like we are drowning in tactics and ad-hoc firefighting, incapable of interpreting the tsunami of change. The world enters a level of complexity that cannot be addressed anymore by conventional, binary, linear thinking.

With all these parts moving at once, we need new tools for monitoring change. We need new capabilities and more non-linear ways of thinking, and openness to new options. We need new tools to forecast, assess, and guide our choices. They should offer richer ways to express our options through visual thinking and other techniques.

This is way beyond flashy hyper-tech bank branches and “punchy-music-cool-sexy” banking apps or product videos. This is about bringing back the analog humanizing aspect into banking. I am not my device. The future of banking is analog not digital, and its focus needs to be on relationships, intimacy, depth, and human connection.

Tomorrow is May 1st, 2012: International Worker’s Day.

And unless you have been living in a cage or other planet, tomorrow is also the day where the Occupy movement is organizing a general strike action across the 125 cities in the USA.

This is organized by the 99%. In the UK however, the “97% Owned” investigates behind the scenes of the ever changing financial system, to uncover how the monetary system provides the foundations for international dominance and national control. Fresh thinking, new ideas and answers to simple questions are squeezed into this 2hr 10minute expose.

Due for release May 1st it features frank interviews and comments from Positive Money, The New Economics Foundation, PRIME, Paul Moore HBOS Whistle Blower, Simon Dixon of Bank to the Future and Nick Dearden from Jubliee Debt Campaign.

97% owned is from the creative team behind Generation OS13: The New Culture of resistance, continuing the distinctive ‘tour de force’ style and artistic interpretation.

Not that i subscribe everything that is said in this video – but i want you to sense the intensity and aggressivity of this movement. It reminds me a lot of what happened in 1977 with the punk movement, or the Flower Power 60’ies, but these were softer more “Peace no War”. This is getting much more confrontational. Check also the comments, as clearly not everybody agrees with the content, the quite tendentious language and music.

Also check-out Simon Dixon (@SimonDixonTwitt), CEO of BankoftheFuture.com, starting off his TEDx talk with some musings on leadership:

“figuring out what you were brought on this earth to do, and then do it”

This resonates strongly in me, see also my latest posts, many of them related to my reflections on what i was meant to be in this world.

Simon explains:

Why we need to change the rules of banking

What will happen if we don’t change the rules of banking

How we can change the rules of banking

His thinking about value is very close to Art Brock‘s ideas on the Living Ecosystem of Wealth (check out www.metacurrency.org). In Art’s model, it’s becoming crystal clear that the majority of investments are purely speculative in nature, and don’t return any value back into the economic system.

Simon is doing a call for:

equality

sustainability

stability

At the end, he also talks on how to change the rules, in essence by training and planting change agents virally in all financial institutions. Sounds familiar to our Corporate Rebels approach where we’d like “to ensure that true change happens virally”, although we are not targeting any specific industry.

Starts crystalizing for me that what Corporate Rebels needs to change is to make our organizations more agile, more fit, more vital, more resilient in creating value rather than extracting value. Now i know why i once read Cradle to Cradle by William A. McDonough (Amazon Affiliates Link) why once again it’s an architect who inspires me. Because it and i was meant to be.

Simon Dixon will launch his own initiative “Banks To The Future” in 30 days or so, as an alternative to bring money to the business without venture capitalists and banks involved.

Another example of “First they ignore you, then they laugh at you, then they fight you, then you win” (Mahatma Ghandi), our theme for last week’s Innotribe in Bangkok.

Simon Dixon looks to me a as good candidate for #innotribe #sibos for the session on “Future of Money”, don’t you think so ? And maybe we should be re-baptise that session into “Future of Value” ?

The last couple of weeks I have been aroused with many ideas and reflections on Personal Digital Assets and on Digital Assets in general.

The journey started some weeks ago with my prezi talk at TEDxNewWallStreet and included my participation to the WEF “tiger team” on Personal Data, where a group of 30 experts are looking at what is needed to make realize the vision of Personal data as a new economic “asset class”. Personal data created by and about people, touching all aspects of society. That group is stitching the pieces together for a framework of business, technical and legal elements that are needed to underpin this vision.

However, the following video from Kynetx was the big aha-moment during my 4-weeks tour on the subject.

I never thought of a Personal Data Store as a “Personal Event Network”.

This changes everything ™

indeed as Phil Windley (@windley), CTO of Kynetx says.

One years ago, there was this beautiful video animation by David Siegel (@pullnews), a great vision of distributed nodes of personal data content talking to each other through API’s.

In the meantime, there is a rich ecosystem of start-ups that are building something very similar as we speak.

Maybe not yet to its fullest grand vision, but definitely going way beyond the traditional concept of a “personal data store”.

Check out leading start-ups such as Personal.com. Btw I dream of one day seeing an integration of Personal.com with an on-line bank. Anybody needing a brokering service here ? 😉

What Kynetx is adding to the mix are three important things:

the “event” based thinking

the prototol for the data-web

Cloud Operating System

Event based thinking:

He really nailed it down for me last time I met him:

In the past we had RPC (Remote Procedure Calls), in essence fire and forget

Then came request/response: you ask for something, and you get it

Now there is the “event-signal”. It does not ask for something, it just says “something’s happened”, and any entity in the network can subscribe to the event and decide itself to do something with it.

For those who remember, in the past we had silo-d email systems. AOL, Compuserve, etc. They did not interoperate. We got rid of those silos when there was a standard protocol, allowing competing commercial and open source servers to talk to each other in SMTP.

We now see the same with data, personal data, social graphs. We have data-silos (Facebook, Google, Bank systems, Health systems, Government systems, etc). What we need is a “Data-Server” and a “Protocol” that allows these data servers to be interoperable.

All this, Phil calls “The Live Web” (Amazon Associates link). He is so excited about this that he has written a book about it.

In other words, start thinking about your “Personal Data Locker” become a “Personal Event Cloud”: your personal data-server in the cloud that can talk and do things on your behalf, can make decisions, interpret rules, etc…

And it can talk to any entity, any node in the web (or at least nodes in any discoverable namespace). In real-time. In multiplexing mode (meaning the node can be both a server and a client).

It suddenly dawned to me that over the last years we have been hyping “The Programmable WEB”, and that if we are serious about customer centric identity or “customer centric” or “personal” whatever, we may wish to start with the “me”.

Suddenly it was flashing in my brain: “The Programmable Me”

“Me” is becoming a node in the grid. We are all nodes in the grid, sending and receiving signals. Like neurons passing an electrical or chemical signal to another cell. And start thinking “synapses” when you talk about the API’s of your Programmable Me.

From Wikipedia:

“Synapses are essential to neuronal function: neurons are cells that are specialized to pass signals to individual target cells, and synapses are the means by which they do so”

The APIs of your “Programmable Me”, of your Personal Event Cloud are indeed the means to make all these nodes interoperable.

Add to this the graph-thinking of Drummond Reed (@drummondreed), Co-Chair of the XDI/XRI Technical Committee of OASIS. Check-out http://wiki.oasis-open.org/xdi/XdiGraphModel and more specifically some of the Powerpoints out there:

Each circle in this drawing represents a node in the grid. I really encourage you to look at this as a graph – this ensemble of inter-connected nodes – as something 3-dimensional, possibly multi-dimensional.

We have all been trained to think hierarchical. Flat files with a root, that sort of thing.

We have to learn to think in graph-models.

You can start anywhere in the galaxy. Every point can be the center of the universe. There is no root. At least, not in absolute terms. Yes, in relative terms with respect to the other nodes in the universe…

A grand vision starts to develop when you realize that the nodes can be any type of entities:

Humans (or their agents)

Circles (like Google Circles) of humans (entities without legal form)

Corporations, non-profits, governmental or educational institution (aka organizational constructs of humans with specific legal form)

We should also include less traditional forms of organizational constructs such as co-operatives, P2P communities, Commons,…

Programs (yes, software code), that perform tasks on behalf of the entities above or that operates as fully independent entities.

Each of these nodes/entities can participate in transactions – or better, “value dances”. “Dance” because the protocol is multiplexing, not one-way request-response.

Of course all these entities will require identity, in the broadest sense, not only URI or ID number, but in the sense of a spectrum, a graph that can be shared in context with other nodes/entities.

Sharing the spectrum becomes the essence of trade

What we are witnessing is a 180° turn in the power balance between client and server, slave and master, buyer and supplier, consumer and merchant.

But look at the subtitle: “When Customers Take Charge”.

I like Doc a lot, but his subtitle may suggest that somebody else is in charge: the empowered customer. I am afraid that we may end-up with another un-balance, where the pendulum has swung the other side: where the customer has an unfair data-advantage versus the merchant. But let their be no doubt that today the merchant has the unfair data-advantage, and I read Doc’s book more like a plea for getting the balance right rather than a socialist rant against establishment represented by the “big boys”, the vendors, the merchants, the silos like Facebook and Google.

In all the discussions about the Empowered Customers, we see classic commerce use cases like buying a book, buying flowers for grandma, etc

But I would like to make the jump to truly balanced financial transactions and what “dances between equals” would mean in that space. I invite you to think about your bank as the merchant, the merchant of financial services, and the consumer as the retail or wholesale customer of the bank.

In such scenario, the fundamental shift in thinking already happens at the Point of Sale (POS). We even have the question the term “Point of Sale”. It stems from an old thinking where the merchant “owns” the customer.

YOU are the point of sale

YOU are the point of data integration!

In the past the POS was the master,

now it will be YOU who is in charge,

or your agent,

the “Programmable Me”.

What if we start thinking about banking where YOU are the point of data-integration? What if your bank would offer you a service that enables you to manage your Personal Event Cloud?

I don’t know how it would look like, but it probably would be something triggered from your mobile phone. It probably would look like one of the Next-Gen banks (Simple, Movenbank, Fidor) with a Personal Event Network out-of-the-box.

Some of these Next-Gen banks are already accepting the CRED of your Social Graph as a much richer (in all senses of the word) basis for “Know you Customer”. Although we probably also have to inverse that: from the captive notion of “know your customer” to the user-centric meaning of “know your bank”. Then we may come back to the “primitive” of the meaning of “bank”: a bench where two people meet to build a relationship of value.

So, the discussion is NOT about the next coolest thing for doing a copy-cat of existing money-transactions through the latest greatest gadget like NFC or Bump, or whatever.

“The thing to keep in mind here” says Crone, “is that NFC was developed more than 20 years ago. It was first deployed 10 years ago. 10 years ago, we didn’t have ubiquitous access to data plans. We didn’t have more smartphones in circulation than feature phones and we had to depend on an ‘offline’ connection for processing payments. But now, there are 124 million households that have more than one device connected to the internet. Typically, that’s a smartphone, but very quickly it’s becoming a tablet.”

Also Christopher Carfi (@ccarfi) starts thinking in this direction in his recent post “Musings in Small Data”. In there, he refers to a video of Jerry Michalski (@jerrymichalski) of the REXpedition doing a demo his “Personal Brain”. (Disclosure: I am member of the REXpedition). The video is titled “Gardening My Brain” and the talk was given at Personal Digital Archiving on February 22, 2012 in San Francisco.

It’s a pity that this talk is in the context of a personal digital archiving conference. Because, in my opinion, we have dramatically evolved from archiving to sharing.

Sharing of information and digital assets is becoming the new normal in this world of Abundance of information.

Christopher Carfi nails it when he says:

As these issues become more widely understood, more individuals will be tracking their own information. Perhaps it won’t be to the level that Jerry has done it in the video above, but it will be happening. This means that we, while wearing our business hats, will need to be developing real relationships with our customers. We need to listen to what they are saying, what they are asking for, and working collaboratively with them in order to help them fulfill their needs. In the best cases, we’ll have built up levels of trust with our customers and will have been given the explicit permission to access our customers’ personal data stores. In doing so, we’ll be able to actually take the guesswork out of the equation that was noted so clearly above in the Facebook example and will, instead, be able to connect directly with our customers’ intentions and deliver value on their terms.

Creating an economy based on the principles of relations is of course at the heart of the REXpedition. It is probably the next territory for competitive advantage beyond the mundane money transaction.

All this is about creating “Relationship Channels”, channels the vendor can tune into of the user has opened the channel.

All the above are of course very much related to our Innotribe incubation project “Digital Asset Grid” (DAG), which is about the sharing of any digital asset with any party.

The real question is then: “Where will value be created when all the connections between nodes have become frictionless?” Mark has some ideas on this, and he describes them as “irreducibles”

“No matter how ‘smooth’ and frictionless hyperconnected commerce becomes, certain frictions in the business world will persist. These represent both speed humps and opportunities. The businesses of the 21st century will find leverage and differentiation by identifying and exploiting them.”

What those “irreducibles” are, you will be able to discover at our upcoming Innotribe event in Bangkok on 26-27 April 2012, where together with Mark Pesce we will have some great interactive learning experiences. Be there, or read the report that we will make on this post-conference.

If you really want to take a meta-view on all this, I believe all the examples above illustrate our species being in search for a deeper meaning, a thicker value in everything we experience:

We are in search for a higher level of consciousness, a further evolution in Spiral Dynamics, in search for a richer value system, much richer than the pure transaction world that is the narrow lens of today

We start looking at companies being nodes in the grid, in fair-trade constellations of equals, trying to maximize the commons and contribution and giving back to society

We want to go beyond the “advertising” thinking of “let’s hit the target with an ad”. We are in search for a better world with more Thick value and less Thin value

We are starting to see the emergence of “The universe as a Computer” as wonderfully described by Nova Spivack (@novaspivack) in one of his milestone posts last month.

All the above is about defining, articulating, and living lives of greater meaning. With the “M” of meaning. Umair Hague (@umairh) already in 2009 called this “Generation-M”, which in essence is anchored in “constructive capitalism”

Generation M is more about what you do and who you are than when you were born. So the question is this: do you still belong to the 20th century – or the 21st?

What I liked about this book is that it encourages you to look at where you are in your life, and to look at it through the “M” lens. The lens of meaning.

I then discover that what I am writing today, what job I am doing, who I am married to, was probably all meant to be this way. Not “meant” in a deterministic way. No, “meant” as everything I have done, the decisions I have made, my architecture studies, my infection by the identity virus, my journey in Leading By Being, etc… all these things have made me who I am.

What if I could capture all this richness about me, and have a tool and an infrastructure to share that on my terms and conditions, in context, and with the parties or nodes in the grid that I choose to? What if I could share my meaning in a programmable way?

I would end up with something called “the programmable me”

After Sibos, Q4 is usually the period of the year when I try to re-boot, to refresh my sources, to be a sponge and take-in new knowledge. It’s when I start painting for the next year. When the themes and trends for next year start emerging.

I wanted to get a much better feel for what this world of alternative and complementary currencies was all about, and decided to join a week-end “Collabathon” organized by Art Brock (@artbrock) and Eric Harris-Braun (@zippy314), the founders of The Metacurrency Project. In the slipstream of the Contact Summit, they wanted to gather the minds to work on NextNet ideas and tools.

From their site:

What is the NextNet? A computing/protocol stack for operating a distributed Internet which enables individuals and communities to transact, self-organize, self-govern and empower themselves to build resilience, sustainability, and thrivability.

It was a small group of people – about 50 or so- gathering that Friday evening. But what a brainpower – and soft-power – in the room! Almost all my twitter heroes were there: it was great and heartwarming meeting many of them in real life.

Friday evening was intro-day. Saturday and Sunday were un-conference days.

The weekend had something “sacred”. The consciousness level of the participants was overwhelming, and Art and Eric introduced the different topics with so much softness and kindness. And every session had some sort or spiritual presence check-in and checkout moment. The location was clean and spacious, with lots of silent breakout rooms, so you could have relaxed but intense conversations. This was about taking quality time with quality people.

Some of you may remember that Art was one of our “igniters” for the New Economies session at Innotribe at Sibos Toronto, but there we only had a couple of minutes.

Here at this Collabathon, Art and Eric gave a 3-hour deep introduction on The Metacurrency project. These guys are so smart, so full of wisdom, so articulated. It was awesome.

The picture above is the essence of the Metacurrency principles. Note how in the bottom left corner, speculative wealth – what Goldman Sachs and others do – is positioned outside of the living systems model. It is fake wealth based on fake growth.

Instead of just describing the model above – plenty of that on the Metacurrency site – I decided in this blog post to transform my notes into some sort of rhythmic at times poetic expression. Step in the rhythm with me:

Currencies are Current-sees

Seas

Sea/See

The flow of value

Experience

The flow of value

Shifts

Capacity shifts

Beyond trading value

Currency as language

Money is one single dimensional sentence of value language

The value of currency is to be able track currents/flows

Currency measures and fails to measure

Money only measures only certain types of values

Spoken and unspoken rules of social norms

Lead to currency

Not currency in isolation

Currency in context

We need to simplify

Not complexify

Make complexity simple in its USE.

Like alphabet

Composable

Letter, words, sentences, compositions

Compositions on-the-fly

Fractal

Composable language

Metaphor of the cow and beef

Once you have beef,

You can’t re-compose the cow,

You can’t go back

The beef misses the whole

Same for milk

The market price of milk has nothing to do with Bessie the cow

With Bessie’s wealth

In context

Wealth in context

Wealth has same root as “wellness”

Value is more contextual, you may not value it, but I may value it

Contextual wealth

We are contextual beings

The Commons of Economics?

“Ecommonics?”

How to account for wealth?

Redo

The company balance sheet

Based on wealth

Balance sheet as momentarily map

The difference between map and territory

The symbols are at the level of the map

Measuring

and missing out something by measuring

Are we missing the context?

Balance sheets in context

Chains of Balance sheets

Balance Chains

Well-being

In context

Worthiness

In context

Worthiness

Currency as an expression of worthiness in something

Worthiness and credibility

Cred

The cred in something

The cred of value attributes of entities

Entities

Humans

Circles

Enterprises,

Governments

Educational institutions

Even software code

Even projects

Reputation of entities

Human reputation

Code reputation

Project reputation

Reputation as a signal of worthiness

Institution design

Institution emergence

Institution intrinsic motivation

Richer measurement

Other than up/down

Like/dislike

Commoditization of relations

The software project

For full details, checkout following Prezi. The guiding principles for the Metacurrency Project are:

Disintermediation of any action, at all possible layer

Composability at all levels

The ladder is about tools, grammars, APIs and standards on one side, and consciousness and new awareness on the other side.

The Metacurrency sees 5 different layers (steps on the ladder), each building upon each other, like emergent systems of small components:

Stream-scapes: a communication composition

Decision making: this is about flows, decision making, event based

Currencies: language for expression of value/wealth

Holoptinets: a new way of visualization of (big) data. Beyond graphs: with the richness of dimensions in an aquarium, a fish tank. The idea is to have an interface that fully exploits the human sensory capacities

OS earth: hat the Metacurrency is after is nothing less than a self-describing computing. And yes, why not be super-ambitious and aim for a redo of the whole computer infrastructure.

There were different sessions on this, the one already more geeky than the other. I particularly like the demo of stream-scapes:

In my own words, it is a sort of EAI-bus, a bus for channels, a channel mixer and filter. Basically, all possible communication channels (Email, Twitter, etc) are blended together in a “scapable distributed database”

A “scape” is a personalized “sculpture” of that blend, reflecting my personal interest and focus. The scape is a grammar. A self-describing grammar at communication protocol level. The idea that people can take existing stream-scapes, adapt/complement them and re-post them in a scape-store for others to re-use. People can build re-usable scapes (grammars) and UIs on top of that.

There was also a good discussion on the “holoptinets”. The initial vision was that the user looks to the fish tank from the outside. Movements of fishes, sounds of water, color, etc. are all expressions of data values. I made some contribution to the thinking by suggesting the user should be “in” the fish tank. Start thinking of concentric fish bowls, each circle representing the types and levels of wealth and the levels of systems integrity of the wealth model.

Is there any traction on all this?

I was witnessing the enthusiasm and passion in the different breakouts of the un-conference. For a lot of this, it is still very early days. And like at Contact Summit, these folks need some sort of coaching on how to “articulate” and “sell” their ideas.

I saw a lot of struggling with even trying to build a first communications strategy on all this. And in my opinion, those stories – if they already exist – are too much inwards looking, too much about the what and not enough about the why.

To get any traction, what needs to get done is to get awareness at senior executive levels. This is something where Innotribe can be instrumental. We can give exposure of these great ideas on the edge of our ecosystem to decision and policy makers. For example, it was a no-brainer to ask Art to fly-over with me to LA to the Compass Summit the next days to be part of our Innotribe Lab on the Future of Value. More about that in a later blog post.

What I found also encouraging was the presence of some Occupy Wallstreet residents. They had a plan to launch an OWS currency. When they saw the richness of Art’s work, they invited Art for a study day on alternative currencies the next Monday.

Because we need to think differently, and not just making a copycat of fiat currencies as a language for pure transaction value only in the left bottom corner of the wealth model.

There was so much richness – wealth – during these two days, that I am exploring the possibility to organize a 1-2 day deep Innotribe conversation with top bankers of our community. And as Art will soon move to Europe, it is a no-brainer to get him over at the SWIFT HQ for a brown bag session for staff and executives.

Next blog will take a bigger helicopter view and will be about the Compass Summit, a blend of technology and values looking at What’s Possible, What Matters, and What’s Ahead.

By now, you should know that on June 1-2 2011, Innotribe will host its first standalone event in Mumbai.

Innotribe Mumbai – Mobile payments: Connecting the unbanked will focus on the opportunities that high mobile penetration presents to take banking services to the historically ‘unbanked’ communities – and explore the ways in which mobile technologies are being used today and can be exploited in the future to enable greater financial inclusion.

Yesterday, we pumped out our first world-wide press-release and we updated the event site with the latest and greatest speakers confirmed. You can also follow latest additions to the program via the Innotribe twitter.

Today, I would like to share some insights in the interactive sessions, the so called “Innotribe Labs”, famous from Innotribe at Sibos.

We have three Innotribe Labs:

On at the end of day-1 on banked-unbanked

Two in the afternoon of day-2: one called “The Mixer” and one called “Mobile Arena”

Innotribe Labs are highly interactive workshops, very well pre-designed and executed by our innovation team under the facilitation leadership of Mariela Atanassova. Whereas the Labs are still under design – trying to leverage the speakers and experts that have committed for these Labs – I can already give you a flavor of what’s going to happen on 1-2 June 2011.

If we can pull it off logistically, we plan to take those interested by bus to the slumps, 2 miles away from the luxury hotel where we hold Innotribe Mumbai. Our plan B is to use video material. It seemed to us that only if you have seen the slumps, you can have a discussion about banked – unbanked.

Nokia will set up a live environment of one their latest project with UBI targeting more than 30,000 villages in rural India. You will be able to experience hands-on what banking the unbanked using cheap mobile device means.

That will be followed by a Lab immersive experience, designed by Innotribe Facilitation Studios.

2 June 2011 – 13:30 – 15:00 Innotribe Lab “The Mixer”

We have the ambition to create “serendipity” or (un)planned encounters. We want to “mix” local and international entrepreneurs in the mobile space and exchange experiences. What works, what not ? What can we learn from each other ? Where does the investment money go ?

We are proud to collaborate with Ashoka. Ashoka is the global association of the world’s leading social entrepreneurs—men and women with system changing solutions for the world’s most urgent social problems. Since 1981, they have elected over 2,500 leading social entrepreneurs as Ashoka Fellows, providing them with living stipends, professional support, and access to a global network of peers in 70 countries.

I have seen the pre-selection of Ashoka Fellows that we’ll have the pleasure to welcome in Mumbai. This will be an awesome experience

We will indeed ask all participants to sit in a big circle, forming a real “arena” discussing mobile payments.

The circle will be segmented in different groups representing banks, unbanked, telcos, platform providers, etc, etc

Each segment or slice will be represented by a pre-assigned spokesman.

The spokesmen will fight in the middle of the arena, in the “snake pit” in the middle of the arena.

The ambition of this session is to come to some recommendation on how to create synergies in this space, to avoid that all parties try to re-invent the wheel, and to see if SWIFT Innotribe can play a role in enabling collaborative innovation.

You got it: Innotribe Mumbai will be a unique experience. Combining an impressive set of speakers with our proven interactive Innotribe Lab format.

As somebody said after our Innotribe Lab at SOFA begin March 2011: “I will never look to SWIFT in the same way, you guys are much more that a network, a BIC code and standards. You are a true innovation community”.

Oh yes, there is one more thing: I have 5 free passes for this event. Send me an e-mail (peter dot vanderauwera at swift dot com) if you want one. They will be given on a first in first out basis. So, you have to be fast !

See you in Mumbai on 1-2 June 2011. May the Innotribe vibe be with you.

Update: just minutes after posting by blog, it was announced that Jack IS back at Twitter, now as “Executive Chairman”. Check-out the news everywhere or here at ReadWriteWeb.

I am getting so inspired by the fabulous Jack Dorsey from Square. Watch this video and the full transcript on Techcrunch. Read David Kirkpatrick’s article in Vanity Fair with the title “Twitter Was Act One”

He makes me think of Liam Gallagher from Oasis. He has something “very British”. He is stylish. The same arrogance. The same pureness. The same design and drive for perfection. And skimming down until only the essence is left over.

One comment reads: “you know what ? Maybe it’s too sounding like the beatles or John Lennon (that was my first reaction). But as a great beatles fan, i’m just glad to see some guys carrying the torch and able to do great music”

And have you seen the interview over the week-end (I think it was BBC) with Liam as part of the launch of the new post-Oasis band Beady Eye ? It seems that the voice of Liam was recorded without any effect, no echo, nothing (not the case in above video).

Pure

The essence

The minimalism of Twitter

Which brings us back to Jack. I believe Jack is the John Lennon of Payments. That Square means for payments what The Beatles mean for music.

Back to the video.

Some quotes from the different articles and transcripts, to get you a good idea how genius this guy is.

“Little Jack Dorsey was obsessed with maps of cities”. Read my recent posts and thinking about the connected economy, the connected company, the connected team and the connected value. They happen also to be the big trusts for our Innotribe at Sibos 2011 in Toronto, later this year

he studied for a year to become a certified massage therapist (Martine will love this)

“Payment is another form of communication,” he says, “but it’s never been treated as such. It’s never been designed. It’s never felt magical. We’re the only payments company in the world that’s concerned with design,”

So the architects designed this gorgeous bridge, but the problem with the Golden Gate is that this is an extremely tumultuous area, if you’ve ever sailed through this or taken a boat through this, the waves are immense. Or surfed through it, which is more dangerous. It’s a disaster, I mean all the weather of the Bay is being forced through this one single point. So, all these elements create this perfect storm of turbulence. It’s extremely deep in the middle and it’s an epic span, so this was not an easy challenge.

And a lot of people think of design, when they hear the word design as visual, something that looks pretty.

Design is not just visual, design is

efficiency

Design is making something simple

Design is epic

Design is making it easy for a user to

get from point A to point B

Reliability is a feature. This is what Brian said earlier, availability, reliability, and staying up, that’s a feature and that’s a product, and it has to be well-designed and thought after and considered, and that’s what we’re doing.

I think I’m just an editor, and I think every CEO is an editor. I think every leader in any company is an editor. Taking all of these ideas and you’re editing them down to one cohesive story, and in my case, my job is to edit the team, so we have a great team that can produce the great work and that means bringing people on and in some cases having to let people go.

This is the bridge I want to cross. [Shows Golden Gate]

This is how I want to arrive at a destination:

This is classy

This is limitless

This is inspiring

This is gorgeous

My dream is to have him at Innotribe Mumbai, where we’ll talk and discuss about Mobile Payments, connecting the un-banked and financial inclusion.

Would really like to hear Jack’s view on design and perfection for that.

Bring Jack Back. To be classy, limitless, inspiring and gorgeous.

SOFA stands for SWIFT Operational Forum Americas, a yearly event targeted at a typical operational audience. This year’s SOFA is on 8-9 March 2011 in NYC. The theme for SOFA 2011 is “Defining the next generation of financial services”.

Innotribe is SWIFT’s innovation initiative. Innotribe’s mission is ‘Enabling Collaborative Innovation’. Part of our activities includes events: existing SWIFT events like Sibos and SOFA, third party events like CPA in Canada and EPCA in Europe last year. It usually translated into a “special” session, with lots of professionally facilitated interactivity.

With Innotribe events we have the ambition to “unpack” stereotypes, myths and hypes. These Innotribe Events are an energizing mix of education, perspective, collaboration and facilitation. Our success factors for this new type event are organized along the following three axes of “opening-up” our traditional ecosystem: audience, content and brand recognition.

So, what’s up at SOFA this year ? We have two things going on:

At the end of day-1, yours truly will give the presentation “How to make babies” a strong metaphor for SWIFT’s Innovation Framework. Prezi version of this presentation is here. Tip: set sound “on”

At the end of day-2, our innovation team will animate a Special Session “The New Thinkers”

Building on the Innotribe @ Sibos tradition of exploring “Tectonic Shifts”, this Special Session will be an energizing mix of education, new perspectives, collaboration and facilitation.

Our goal is to stimulate the generation of new ideas by bringing together a powerful mixture of audience members and by enabling freedom of discussion – allowing the conversation to take the participants into any and all areas that open up on the day.

We believe strongly in the potential

of unexpected encounters,

and the magic that can happen

when people from

different background

are brought together

So the innovators and change agents of our industry will be invited to join the SOFA audience (and also to join us in Toronto for Sibos 2011 in September), and we hope this will foster exciting new discussions between them and the traditional SOFA attendees.

Ideas do not typically come out of the blue. Rather, they are usually variations of existing ideas. Sometimes, simply looking at a familiar idea from a different perspective can spark a new idea or the combination of existing ideas to achieve new goals and create radically different value propositions. All the topics we propose to discuss during this Innotribe Special Session at SOFA are also potential subjects to explore in Toronto – but we are looking for your feedback to tell us if these are the right ideas to stimulate your creative thinking!

Presentations from five great modern thinkers will culminate in an interactive exchange between the SOFA audience and the speakers, led by Innotribe facilitation champ Mariela Atanassova. The audience will be able to drive the discussion according to the themes that most interest them – ensuring everyone will have an opportunity to collaborate in the innovation we hope this session will stimulate.

Here are The new thinkers:

Venessa Miemis (http://emergentbydesign.com/about/): Free agent, Master in Media Studies at the New School, NYC, futurist and digital ethnographer, researching the impacts of social technologies on society and culture and designing systems to facilitate innovation and the evolution of consciousness. Venessa will update us on The Future of Money project (world premiere at Sibos 2010) and The Future of Facebook, a new research project sponsored by Innotribe as Corporate Patron.

Brian Zisk: organizer of the Future of Money & Technology Summit in San-Francisco (www.futureofmoney.com). Brian will summarise the findings of the Summit that took place on 28 Feb 2011. Psssst ! If you still want to go to Brian’s event, go the the registration page at ttp://futureofmoney.eventbrite.com/ and use the discount code “Innotribe”.

Stowe Boyd (http://www.stoweboyd.com/ ): probably THE authority on Social media, Stowe is a Social Philosopher and Webthropologist from NY. His work focuses on social tools and their impact on media, business, and society. In 2011, Stowe is focused on a new line of research: Social Cognition. This research is co-sponsored by Innotribe, and we hope to share the final results at Sibos 2011 in Toronto.

Kevin Slavin (http://about.me/slavin): also from NY, Kevin is founder of AreaCodeInc (recently acquired by Zygna, the undisputed leader of Social Games). Kevin will talk about the New Future and “Those algorithms that govern our lives” – including our personal finances!

(picture from Dave Gray’s blog)

For the interactive part, we will organise the session around the organic growth aspects of cities. I have written about this before in my post “How to make babies”, and recently there was a fantastic post by Dave Gray on “The Connected Company”. We invited Dave to SOFA as well, but he unfortunately could not make it.

Dave’s post is a fantastic post – and as far as I am concerned – one of those game changing post already for 2011, and I will definitely come back to it later.

Dave for example says:

And today, thanks to social technologies, we finally have the tools to manage companies like the complex organisms they are. Social Business Design is design for companies that are made out of people. It’s design for complexity, for productivity, and for longevity. It’s not design by division but design by connection.

")