If you can’t get enough of these and want more than 5 articles, I have created an extended version of Petervan’s Delicacies in REVUE. If you want more than 5 links, you can subscribe here: https://www.getrevue.co/profile/petervan

Many of my readers know I was trained as an architect. Some of the rhythms, insights and passions of that profession continue to weave into my work and my sense making.

Just over the weekend, I completely randomly bumped into a very well done interview with star-architect Rem Koolhaas in Flanders’ business newspaper “De Tijd”. It’s in Dutch, but I found it so inspiring that I translated the juiciest chunks of that interview, with some personal context around that.

Rem Koolhaas (70) founded the Office for Metropolitan Architecture (OMA) in 1975. Besides its headquarters in Rotterdam, the agency has offices in New York, Beijing, Hong Kong, Doha and Dubai. He is also a professor at the Harvard Graduate School of Design and wrote important publications on architecture, such as ‘Delirious New York’ (1978), “S, M, L, XL (1995) and ‘Content’ (2004). In 2000 he was awarded the Pritzker Architecture Prize, the Nobel Prize for architecture.

It was Dasha Zhukova, the 34-jarige spouse of Russian multi-billionaire Roman Abramovich who approached Koolhaas to build “her” museum. Thanks to the deep pockets of her husband, she ensured herself this way of her own name and fame in the international jetset and art scene.

I really encourage you to watch this great promo-video of the museum. It is so inspiring when you start thinking about musea as educational spaces. Look at the wondering faces of the kids in that video. Think on how educational immersive experiences are becoming so key to our understanding and sense making. The Garage Museum is run by the Post-Soviet generation and that is so refreshing. And – surprise – it includes fragments by performance artist Marina Abramovic.

Her work explores the relationship between performer and audience, the limits of the body, and the possibilities of the mind. Active for over three decades, Abramović has been described as the “grandmother of performance art.” She pioneered a new notion of identity by bringing in the participation of observers, focusing on “confronting pain, blood, and physical limits of the body.” (from Wikipedia).

It is a coincidence – or probably not – that performance, improvisation and new notions of identity cross my path again, and makes me reflect again of my work as event-creator evolving gradually into experience, romanticism and mystery.

But back to the interview. The journalist kicks off with an observation about the label of “star-architect” and how that is associated with neoliberal money-grubber who designs antisocial icons for the private super rich.

Rem Koolhaas reacts:

“Since the beginning of the 21st century, there is increasing attention to an ever smaller group of architects, of whom one expected to produce ever more spectacular buildings. Especially in high-rise commercial noticeable increasing pressure to make extravagant, rare designs. “

“Since the triumph of the market economy, the relationship between the public and the architect is cut. The takeover of the market economy in the architecture was harmful. The architect can no longer identify as someone who serves the public interest. Previously our inventions benefited humanity. Now that’s gone, like a tablecloth is suddenly pulled away.”

“While architecture previously revolved around the creation of community, to live together, the emphasis on selfish icons wipes that away. Cities can no longer exert as much influence as before, when they had enough money to build projects.”

It makes me think about the work of Christopher Alexander – my all time favourite – who protests against efficiency in architecture and the loss of appreciation for patterns, beauty, and the “quality without a name– QWAN”. See elsewhere on my blog, like here on “The battle for beauty”. Like Alexander, Rem Koolhaas is at least as famous as a thinker and writer on architecture.

“I think an architect must be a change expert, because you have to shape change. Therefore, you must know what is happening in the world. Before I became an architect, I was a journalist. And actually I’m still investigative journalist. I observe. My life is one big string of anthropological and sociological explorations. I’ve always had a particular attention to what is neglected. So I wrote my book about New York in the late seventies, when everyone had written off the city.”

He also confirms some of the insights that digitization of architecture – but I would expand that to any form of making great work – creates some fundamental flaws in creativity.

“I think some architects have a very simplistic look at the digitisation. For instance, they believe that 3D printing will provide free creativity. That is a myth. Therein lies a fundamental fallacy about architecture. Architecture is not at all about letting your imagination go. You must confront your imagination again and again with the request and desire of your customer.”

And then on privacy, something that becomes most tangible when you are at home, in your house, in your bedroom.

“It dawned on me last year when I was curator of the Venice Architecture Biennale. We have reconstructed the history of building elements, such as wall, floor, heating, and so on. We realized that all of them are on the verge of changing status. Take the thermostat. That used to be a thing that you checked. Now that gives your data to the energy supplier. Such a smart thermostat knows when you leave the house and when you come home again. Before you know it, sensors that follow you anywhere in your home surround you”

“We live in a world which is so addicted to comfort it as undermining our freedom. The dividing line between comfort and repression is thin. We submit ourselves to a huge monitoring system that records all of our movements in a building. We seem almost happy that we have no privacy anymore. For someone of my generation is that strange because we were still in the streets in the seventies to defend our privacy. “

Picture of Lone Swimmer by Sterling67

“I travel a lot, and I find that very inspiring. And above all gives me a great deal of privacy. Like swimming, though. I swim every day one kilometer, wherever in the world I am. “

From time to time, I am invited to give a keynote presentation. More and more i am adding multimedia elements to that: video, audio, even silence. This transmedia approach is also something that keeps inspiring me when doing my day job, where i am architect and content curator of “events”. I always say that i am not in the “events” business but in the business of creating high quality feedback loops to enable immersive learning experiences. That’s quite a different ballgame.

Some fans believe that what I do with our flagship Innotribe@Sibos is where i put the bar. It is not.

It is my starting point.

I really would like to go much further in touching my audience at another, additional level than purely the cognitive level. That’s why i believe a multi-sensory, more intimate, even business romantic experience is needed.

That’s why i love so much the work of Tim Leberecht, here in a recent talk at TEDxIstanbul:

I strongly recommend you watch this talk for the full 18 minutes. And read the book it is based on.

Tim Leberecht, author of the book The Business Romantic and chief marketing officer of global design firm NBBJ and, worries that big data, algorithms, and self-tracking technologies are engineering the romance out of our lives. He argues that we can find and create more meaning, and even magic, by designing experiences that connect us with something greater than ourselves. He contends that we all long for moments that are powerful precisely because they are inexplicable, such as acts of collective generosity, random digressions, and exuberant passions, and even the beauty of losing control.

He is referring to “Unexpected moments of beauty, awe and wonders, the detours and digressions, the cracks of imperfection, that make a heart speed faster, adrenaline rush, moments in which we loose control, and fall in love with everything.”

When was the last moment in your professional life when you had an experience like that?

It seems that only the measured life is a good life. Optimized by algorithms. I don’t believe in that anymore. There must be something better, more intimate, more unique, more transient, less about scaling and optimizing.

It’s not an easy read, but Oliver Burkeman from The Guardian reviews: “Crawford has a point … adverts are everywhere, so much so you have to pay to escape. There are real benefits to silence. No great book, or idea comes without a degree of silence. Independent thinking is not possible without it. Perhaps this is why so many corporations and institutions demand our attention – and why we should protect it Scotsman Incisive. It’s philosophy as an intervention in issues of the day.”

And The Chronicle of Higher Education raves: “The most cogent and incisive book of social criticism I’ve read in a long time: accessible, demanding, and rewarding. Reading it is like putting on a pair of perfectly suited prescription glasses after a long period of squinting one’s way through life”

The book describes the big disconnect between our agency (or the illusion of it, by seemingly being in control by clicking some buttons on an app) and the result of our agency, the work, the piece of craftsmanship, that piece of art.

That’s why i deeply refuse to see my work “as a job”. Work should equal meaning should equal passion should equal Art. The artist’s way…

That’s why i subscribed again to Art School last year, and i just registered again for the 2015-2016 season. Last year was about drawing, next year will be about painting.

Own artwork @petervan 2015 - pencil on paper and some water diluted black chinese ink

That’s why i carved out some quality time for myself on Fridays, when i experiment with art, sound and poetry. And i installed a small studio in my atelier at home, with a MIDI keyboard attached to my Mac, running Garageband and Ableton Software. I also got myself a “Push”, a special hardware device to play music and create sound landscapes in Ableton.

So i started thinking about what it would take to evolve my presentations into some sort of performance, where i only use my own artwork, my own self-composed sound landscapes and my self-written poetry. And do it LIVE! Standing in full vulnerability.

And what would a trailer for such a live performance look like? Here is a little experiment… The trailer is just an existing iMovie template tweaked with my own artwork.

I showed it to some friends, and i was surprised how much a little thingie like this can create emotional reactions. Somebody else wanted me to do some commissioned work to create an immersive learning performance for a marketing event in 2016. Yet somebody else wants me to completely re-invent their executive off-sites to move them away from the boring flipcharts, whiteboards, post-its, scribing, and gamification tricks. And move them into deep intimate and almost zen-like retreats with tailer made, unique and transient multi-sensory experiences to create high quality connections of human beings on a mission for genuine and positive impact.

All these formats create a new type of scarcity, experiences that we can’t fully posses, experiences that don’t last, experiences that we don’t fully comprehend. They restore friction and doubt in a world of certainty, knowledge, and seamlessness-ness.

Formats where it is not about rapid prototyping, nor about fast iteration tracks to find a solution for a problem. We have to get out of problem solving mode. We already do that the whole year long. I believe we are hungry for a higher quality of being truly present. What Tim Leberecht calls:

“Being Thickly Present”

Maybe i am onto something that may lead to another level of awareness and articulation of corporate narratives beyond the hollow mission statements. Entering a new age of enchantment, in search for something bigger and more valuable than all that what can be measured. The beauty of things that don’t scale. Beauty keeps on chasing me. I wrote about it in “Confused by Beauty” and “The Battle for Beauty” featuring once more The Business Romantic.

A generational shift is underway, which is challenging and reinventing notions of trust in financial services. The Millennial Generation, comprised of those people born between 1982 and 2004 (average age 22), lies at the heart of this shift.

A couple of months ago, i spotted the twitter stream and website of Wharton FinTech, the first student-led FinTech initiative committed to education, career development and idea promotion by connecting innovative, established, disruptive and proven FinTech enterprises with students and industry professionals.

I got into a conversation over Skype with Daniel McAuley and Steve Weiner, the two co-founders of Wharton FinTech, and discovered a rich community of young Wharton MBA students who were passionate about FinTech. They organise study tours in the Valley and elsewhere, have a solid blog, and more importantly have a refreshing view on which financial services resonate with Millennials and which not.

We started an online collaboration to produce a research paper, and after a couple of iterations quickly decided that the underlying theme had to do with trust. A different kind of trust.

Trust is the most important currency in finance. It is fundamental to the smooth running of every financial system in the world, and that is always likely to be so. However, a generational shift is underway that is challenging and reinventing notions of trust in financial services.

Growing up during the global financial crisis and a sluggish period of recovery thereafter, the Millennial Generation is particularly mistrustful of established financial brands and institutions. The effect of this generational shift has been explored by a number of groups, including the innovation group, Scratch. Their Millennial Disruption Index concludes that banks are most likely to be disrupted by Millennial consumer preferences, and are facing massive challenges in terms of approach towards customer acquisition and user experience.

Millennials believe that the way we access money and pay for things will be completely different five years from now. But how do companies understand what trust really means to this generation, and more importantly, find ways to earn and retain it?

The paper explores three main themes:

Trust in technology: Millennials trust technology rather than face-to-face relationships and the traditional ‘bricks and mortar’ on-premises user experience. They want entirely new digital products that are relevant to their daily lives. However, there is a fine line between trust in technology and over-reliance on it, and information and identity security is an area of risk that needs to be managed.

Trust in networks: FinTech startups built on the back of social networks have a distinct advantage over incumbents when it comes to customer acquisition. By focusing on user experience and viral or ‘word-of-mouth’ marketing, these young firms are often outperforming their better-funded rivals. For those financial services firms looking to gain market share within the Millennials segment, this is an extremely important approach to master.

Trust in social causes: Millennials demonstrate a stronger likelihood to buy a product from, or indeed work for, a company with a defined social or environmental mission. They trust companies with social or environmental objectives more than those that are perceived as operating solely for profit. While declaring affiliation to a social cause can attract customers and improve engagement, companies must be careful not to mislead Millennials – they tend to do their research to make sure a company’s claims can really be justified.

Socio-economic and generational dynamics play a critical role in the evolution of financial services. As companies reinvent the way people interact with their money, finance is becoming faster, cheaper and more efficient for individuals and businesses.

The paper can be downloaded here (PDF) and provides valuable guidance on what financial services companies can and should be doing to capitalise on this major generational shift in consumer preferences, and create new opportunities for growth.

Together with Power Women in FinTech, Millennials will play an important role in this year’s Innotribe programme at Sibos, taking place in Singapore from 12-15 October 2015. In preparation for the event and the discussions that will happen onsite at Sibos, the paper examines how the Millennial Generation will help shape the future of finance.

Week-25 of Delicacies: What a rich week that was. But i stick to max 5 articles that i found interesting and worth re-reading. Handpicked, no robots. Minimalism in curation. Enjoy!

On Friday, June 26 at noon Central European Time, we kicked off our 24 hour Rebel Jam 2015. The recordings of all the sessions are now available here (*). There was a lively twitter stream: check out hash tag #rebeljam15

(*) We had a small technical glitch for the last sessions of the Rebel Jam, resulting in some recordings missing. We are contacting the speakers 1-1 to re-record their session. Sorry for that.

Rebel Jam 2015 was sponsored by RELEVENTS, committed to enacting a movement of positive change in the business community.

And together with RELEVENTS, we are proud to announce the first Rebel Jam LIVE!, an event pavilion where i community will meet for the first time since its existence in a face to face setting. Mark your calendars!

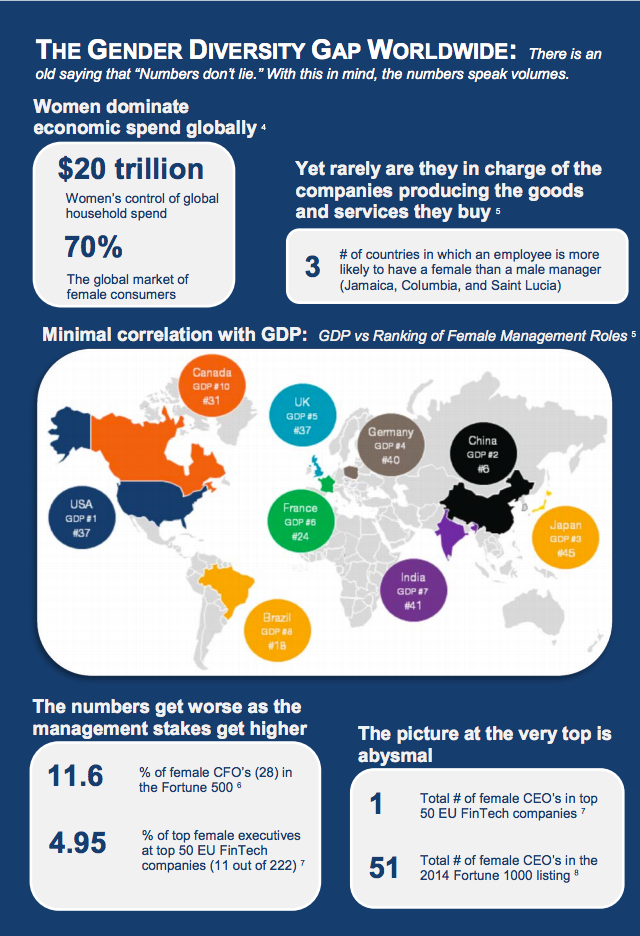

While technology and business models are changing fast, the issue of gender diversity in financial services – particularly at senior leadership levels – is still lagging behind. A Financial News analysis of Dow Jones Venture Source and Factiva data reveals that, of the 20 European FinTech companies that received the largest venture capital investments in 2014, none had a female chief executive.

A couple of months ago (Nov 26, 2014), I got a DM tweet from @sammaule saying “Been asked to put together a list of top 100 women in FinTech globally for conference in March. Looking for your input.”. I reached out to Sam and suggested we’d make this a major design theme for Innotribe Sibos 2015, and produce a joint whitepaper on Powerwomen in FinTech.

It was the start of a fantastic collaboration with Sam and Christine Duhaime @cduhaime from Digital Finance Institute in Canada, culminating in the release of the paper on June 3, 2015 during at Digital Finance 2015, the first Canadian FinTech conference, in Vancouver.

We did not want it to be yet-another-list. We did not want it to be another girl-geek-power list. What we wanted was a list of women who make a difference in financial services. Whether they were having C-level roles in their organizations or were change agents deep in the fabric of their institutions. Whether they came from big or smaller financial institutions, startups, investors, or VCs. We had the ambition to have a worldwide list.

We compiled all existing lists. Did crowdsourcing via twitter and other social media. We had a good list, but found it a bit light for regions such as South America, Africa, and Asia. We reached out to our contacts in those regions, and got additional suggestions.

We ended up with a list of 437 Powerwomen in Fintech, and could have kept going.

The paper draws upon existing research to highlight the reality of today’s situation in FinTech, and it provides recommendations to achieve and accelerate greater gender balance within the industry. A selection of interviews and profiles sit alongside the index, highlighting and celebrating the success stories of just some of the inspiring women who are leading the way and serving as role models to others.

End August we will do an update, and have some more in-depth interviews with 25 Powerwomen from the list.

The paper serves as an eye-opener on the gender diversity gap, in advance of the debate that will continue at Sibos in Singapore, from 12-15 October. Diversity will be one of the main topics covered by the Innotribe@Sibos 2015 programme. A number of the inspirational leaders featured in the Power Women in FinTech index will be involved in Innotribe sessions to discuss the findings of the paper, and make sure the voice of women is heard.

The paper can be downloaded and is a compelling read for anyone involved in the financial industry and beyond.

Since then we all have seen that story unfolding, up to some months ago where the slides from CB Insights went a bit viral.

This is looking at the home page of Wells Fargo, but i have seen versions for HSBC and others. The message here was that we witness the disaggregation or uberization of financial services and that the new capability is to be able to horizontally source pinpoint functionality and mix and match these into new experiences. That was Fintech 1.0. It’s a vibrant startup space, and for sure full of investment, accelerators and incubators. But it’s boring and missing the big picture.

The new paper helps us seeing the big picture. From the foreword:

“Many fintechs have succeeded but today they are still operating only at the edges of banking. To help engineer more fundamental improvements to the banking industry, they must now be invited inside, to contribute to reinventing our industry’s core infrastructure and processes. That can succeed only as a collaborative endeavour, with banks and fintechs working together as partners.”

There are many examples in the paper that illustrate that. Here is an example of streamlining securities settlement:

However, many financial institutions are still stuck in the pre-Fintech 1.0 era: they just start to see the light that Sean Park was shining on the vertical disaggregation of financial services. That is seven years after the first signals were clear in the market. They simply have not adjusted their clockspeed to the 21st century economy speed.

Other institutions were more pro-active and created corporate investment funds (some of them 100-200M USD or more) and/or partnered with accelerators and incubators. Probably most of that money is gone now. And to be honest, i don’t see much innovation that is actually shipped into the market. At best we ended up with some well advanced prototypes and we struggle to get them out of the sandbox. To quote myself: “Innovation that does not ship into the hands of a paying customer is fantasy”

The new paper shifts the innovation agenda. All the problems and opportunities in the paper are of a collaborative nature. Maybe not in a way that the authors intended.

It looks from the paper that the conversation with startups has moved on from competing with the banks to collaborating with the banks. I can subscribe to that, it’s a clear message i have heard from the startups and the banks during all the startup competitions i have been invited to for coaching and judging.

But many of the problems and challenges in the paper can only be solved through a collaborative effort by the industry at large

Just a couple of days ago i was in a meeting with heads of innovation of major financial institutions. One of the messages was that we as an industry have to be more bold, set our competitive agendas asides and join forces to compete with the next generation of competitors that are not the startups at the edges but big technology companies with very deep pockets and with the super disruptive capability of becoming ecosystem/platform orchestrators where banks will rather be the slaves than the masters.

FinTech 1.0

FinTech 2.0

Products

Processes

Tactics

Strategy

Doing the existing better

Do brand new

Efficiency game

Value creation game

At the edges

At the core infrastructure

Key Performance Indicators

Key Capability Indicators

Vertical

Horizontal

Competition

Collaboration

Prototypes

Shipped Products

Transactions

Enable Commerce

The new paper inspires me. I got somewhat bored of hearing the startups doing the same standard pitches, and attacking/leveraging/whatever one particular area of financial services. I am hungry to see startups wanting to play the big game. The game of infrastructure. Of re-inventing processes rather and putting lipstick on or around the pig.

In that sense FinTech is dead. The game is up. It is about enabling commerce. It’s about better banks and better banking with a greater societal awareness to enable commerce and supply chain. Not just transactions in the back-office.

Week-23 of Delicacies: Rich harvest this week. But still max 5 articles that i found interesting and worth re-reading. Handpicked, no robots. Minimalism in curation. Enjoy!